Many patients may assume they no longer have financial responsibility for their medical bills once their insurance starts covering costs. The reality sets in when the bill arrives & they see hundreds or even thousands owed to their name.

This typically happens due to coinsurance, which refers to the distribution of medical expenses between the patient and the insurer after the deductible is met.

As one of the biggest drivers of unexpected healthcare bills, it is essential to understand how coinsurance works to avoid potential financial surprises.

What Is Coinsurance?

Coinsurance is the percentage of a medical bill that a patient must pay after meeting their deductible. The remaining cost is covered by the insurance provider.

For example, in an 80/20 coinsurance plan:

→ The insurer pays 80%.

→ The patient pays 20%.

Coinsurance is not a fixed amount. In fact, it is cost-dependent, which means the higher the total medical expense, the higher the patient’s share.

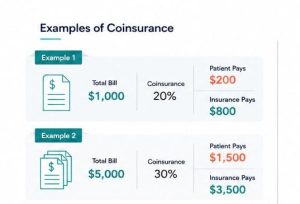

Examples of Coinsurance

Coinsurance becomes easier to understand when applied to real numbers.

Example no. 1

Let’s say the total bill is $1,000 and the deductible has already been met. If the coinsurance is 20%, that means the patient pays $200, leaving insurance to cover the remaining $800.

Example no. 2

If the total bill is $5,000 and coinsurance is 30%, the patient will pay $1,500, while the insurance pays $3,500.

Coinsurance plays a major role in overall healthcare cost-insurance since expenses can increase significantly for hospital stays, surgeries, or advanced imaging.

Importance of Coinsurance in Medical Billing

A health plan coinsurance is not merely a patient cost. Instead, it directly affects revenue collection and payment timelines at the provider’s end.

It determines:

- The patient’s financial responsibility after insurance has been processed.

- How much must providers collect from patients…

- Payment delays due to confusion or disputes.

For patients, coinsurance is one of the most common reasons behind the financial burden of medical bills.

Therefore, conditions associated with coinsurance must be clearly communicated beforehand to avoid billing issues and improve collections.

How Does Coinsurance Work in Health Insurance?

For a better understanding of how does coinsurance work in health insurance, providers offer a structured process.

- The patient pays 100% of medical costs until their annual deductible is met.

- Coinsurance starts applying after the deductible.

- Costs are shared between the patient and insurer based on the plan percentage, such as 80/20 coinsurance.

- Once you have reached yearly limit for out-of-pocket costs, the insurance provider covers 100% of medical bills for the rest of the year.

What Is Coinsurance After Deductible?

Coinsurance after deductible simply means that once the patient has paid their deductible, which applies annually, they begin splitting costs with the insurer.

For example:

The annual deductible in a patient’s insurance plan amounts to $1,000, and the coinsurance percentage is 20%. The patient will initially cover their medical bills all by themselves until meeting the deductible.

Once it is finished, the insurance starts helping as per the predetermined coinsurance percentage. For every medical bill, the patient pays 20%, while the remaining 80% will be covered by the insurer.

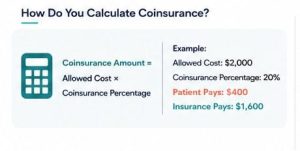

How Do You Calculate Coinsurance?

Coinsurance in healthcare insurance is calculated using a simple multiplication of the total allowed cost-insurance of medical services by the predetermined percentage (e.g., 20%).

Coinsurance Amount = Allowed Cost * Coinsurance Percentage

In the aforementioned formula, allowed cost or allowed amount refers to the maximum price the insurer agrees to pay for a medical service. Coinsurance percentage is the portion of the medical bill owed by the patient after meeting the deductible.

Example:

- Allowed cost: $2,000

- Coinsurance percentage: 20%

- Patient pays: $400

- Insurance pays: $1,600

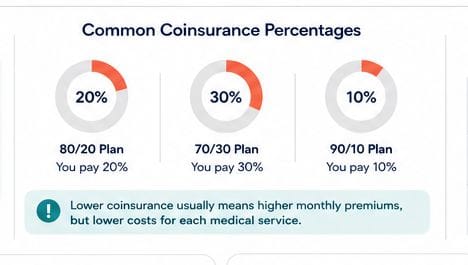

What Are Common Coinsurance Percentages?

Common coinsurance percentages are typically expressed as a split between the insurer and the patient. Though they vary depending the insurance plan, common structures include:

- 80/20 plan: Patient pays 20%.

- 70/30 plan: Patient pays 30%.

- 90/10 plan: Patient pays 10%.

If the coinsurance percentage is low, it means the patient is paying a higher monthly premium amount for insurance. In these cases, the patient pays less for each medical service.

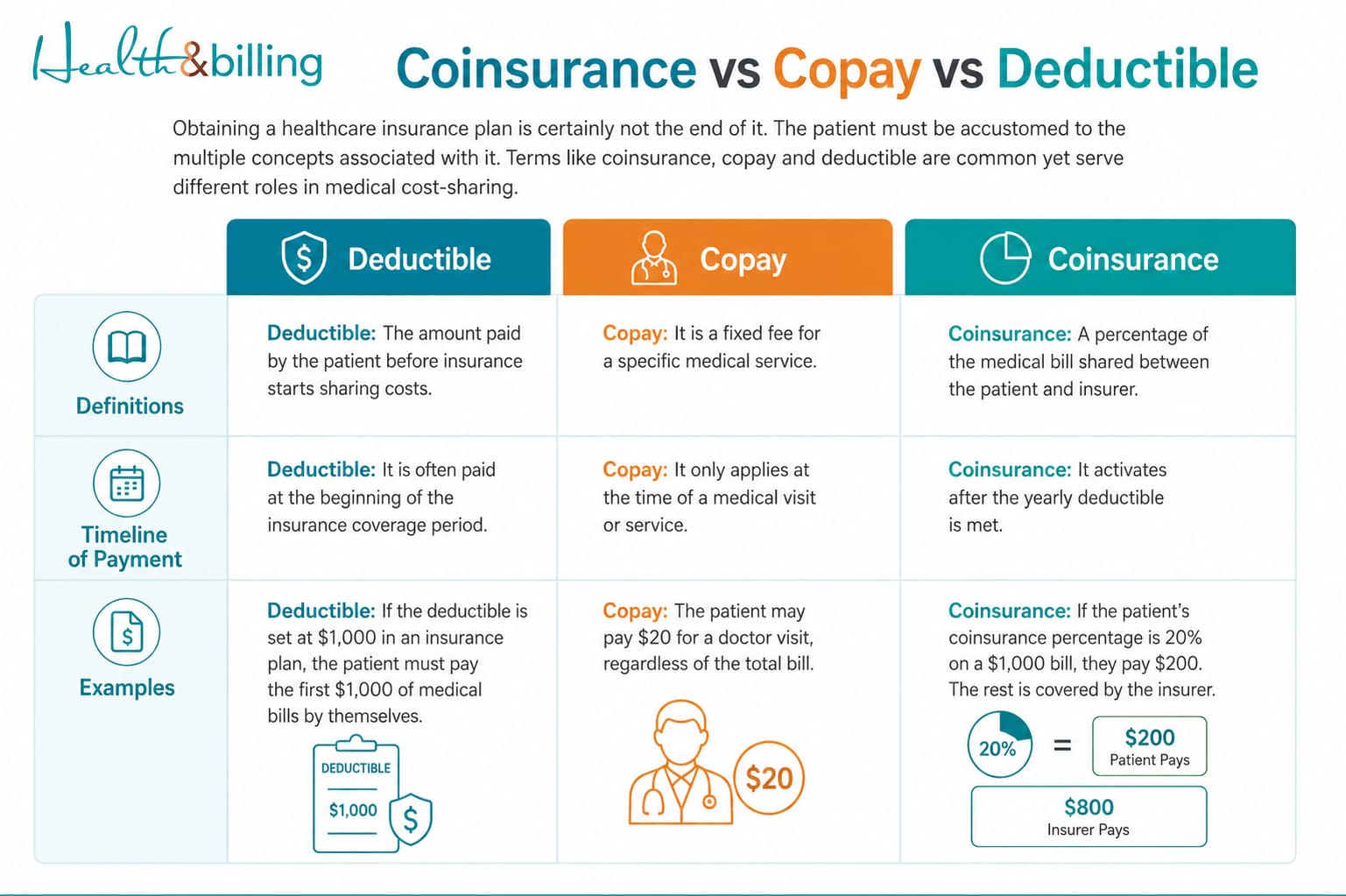

Coinsurance vs Copay vs Deductible

Obtaining a healthcare insurance plan is certainly not the end of it. The patient must be accustomed to the multiple concepts associated with it. Terms like coinsurance, copay and deductible are common yet serve different roles in medical cost-sharing.

→ Definitions

Deductible: The amount paid by the patient before insurance starts sharing costs.

Copay: It is a fixed fee for a specific medical service.

Coinsurance: A percentage of the medical bill shared between the patient and insurer.

→ Timeline of Payment

Deductible: It is often paid at the beginning of the insurance coverage period.

Copay: It only applies at the time of a medical visit or service.

Coinsurance: It activates after the yearly deductible is met.

Copays often apply from day one, while coinsurance typically waits for the deductible.

→ Examples

Deductible: If the deductible is set at $1,000 in an insurance plan, the patient must pay the first $1,000 of medical bills by themselves.

Copay: The patient may pay $20 for a doctor visit, regardless of the total bill.

Coinsurance: If the patient’s coinsurance percentage is 20% on a $1,000 bill, they pay $200. The rest is covered by the insurer.

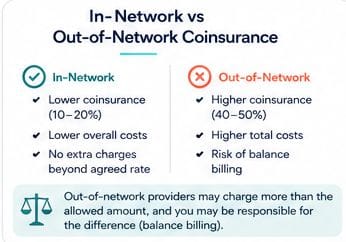

In-Network vs Out-of-Network Coinsurance

Coinsurance is not the same for every healthcare provider. Instead, it depends heavily on whether they are in-network, i.e., they have a contract with the patient’s insurance company, or out-of-network, i.e., the provider does not have a contract with the insurer.

In case of in-network co-insurance, the healthcare provider may agree to provide services at pre-negotiated rates.

It typically means:

- Lower coinsurance percentage (e.g., 10-20%).

- Lower overall costs.

- No extra charges beyond the agreed rate.

For out-of-network providers:

- Coinsurance percentage is typically higher (e.g., 40-50%).

- Higher total costs.

- Risks of extra financial burden.

With out-of-network care, the provider may charge more than the allowed amount on the patient’s insurance plan. This is called balance billing.

For example, the hospital charges are $1,500. The allowed amount for the particular medical service is $1,000 on the patient’s insurance plan. Meanwhile, the coinsurance percentage is 50%. The patient pays 50% of the $1,000, i.e., $500 as well as the extra $500 of the doctor’s charges. This way, the insurance only covers $500 of the total medical bill for an out-of-network provider.

Common Mistakes People Make About Coinsurance

Proper understanding of coinsurance is essential for patients to avoid unexpected expenses linked to their medical bills. Some of the common mistakes they make about coinsurance include:

- Many people may assume that insurance pays everything once the deductible is met. However, coinsurance means the patient still shares a percentage of the cost.

- Patients sometimes confuse coinsurance with copays, which is the fixed amount they pay on a doctor visit.

- Patients may end up bearing larger medical bills if they ignore the higher coinsurance rates associated with out-of-network providers.

- Since coinsurance applies to high-cost procedures and calculated on the total cost, it may result in high out-of-pocket payments for patients.

Out-of-Pocket Maximum and Its Relation to Coinsurance

In medical billing, the out-of-pocket maximum is the annual limit of what a patient must pay for services typically covered in their healthcare insurance plan.

Once this limit is reached, the payer covers 100% of the covered costs and coinsurance no longer applies.

For example, if the out-of-pocket max is $6,000, patients are not required to pay any coinsurance payments after reaching it.

Out-of-pocket maximum aims to provide financial protection to patients against extremely high medical expenses.

How Does Coinsurance Affect Your Medical Bills?

In medical billing, coinsurance plays a major role in determining actual healthcare costs. It especially carries a substantial financial impact for high-cost services and out-of-network care.

If a patient’s health plan shows higher coinsurance, the patient is responsible for greater out-of-pocket expenses. It also poses increased financial risk on them for expensive procedures.

In the case of lower coinsurance, the costs are much more predictable and manageable since the patients are responsible for a smaller portion of each bill. It is often due to higher monthly premiums, where they pay more upfront for the insurance plan.

Bottom Line

Coinsurance is a core component of health insurance that defines how costs are shared between the patient and the insurer. Confusion around it often leads to billing delays and patient disputes.

Partner with Health & Billing to get accurate cost breakdowns and streamlined billing support for your practice.

FAQs

Do I pay coinsurance before deductible?

No, coinsurance typically applies only after you have met your deductible. Before that, you usually pay the full cost of medical services.

What is a good coinsurance percentage?

A lower coinsurance percentage, such as 10-20% is ideal because it means you pay less out of pocket for each service.

Can coinsurance be avoided?

Coinsurance usually can’t be avoided if you have obtained a healthcare insurance plan. Thus, it is often recommended to choose plans with lower coinsurance percentage.